AR5 Working Group II

Published on Mar 30, 2014 • IPCC Fifth Assessment Report - Working Group II - Climate Change 2014: Impacts,

Adaptation, and Vulnerability

AR5 Working Group II

Published on Mar 30, 2014 • IPCC Fifth Assessment Report - Working Group II - Climate Change 2014: Impacts,

Adaptation, and Vulnerability

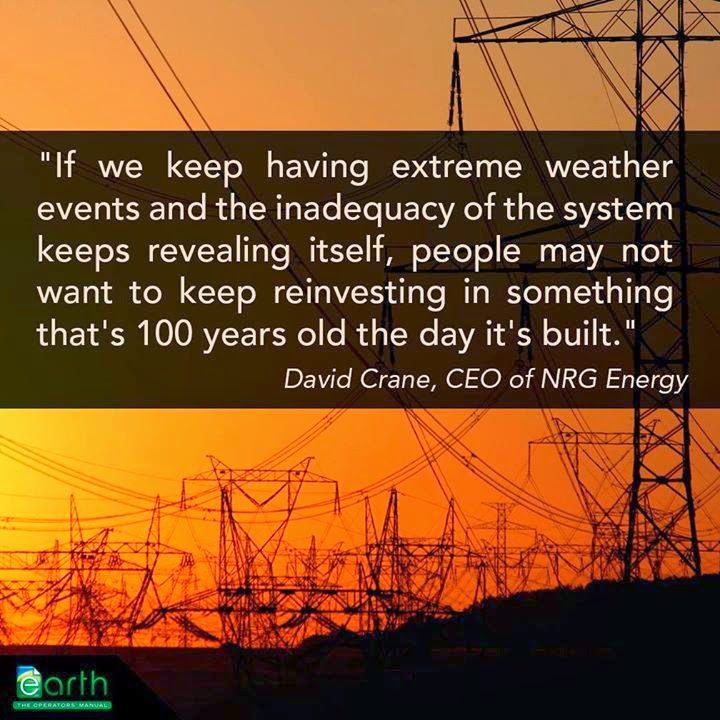

ETOM Quote of the Day:

"If we keep having extreme weather events and the inadequacy of the [electrical utility] system keeps revealing itself, people may not want to keep reinvesting in something that's 100 years old the day it's built." - David Crane, CEO of NRG Energy

Crane sees a future not in centralized utilities, but in distributed generation - solar panels on every home.

http://ow.ly/lQ1dP

In a new book, former oil geologist and government adviser on renewable energy, Dr. Jeremy Leggett, identifies five "global systemic risks directly connected to energy" which, he says, together "threaten capital markets and hence the global economy" in a way that could trigger a global crash sometime between 2015 and 2020.

According to Leggett, a wide range of experts and insiders "from diverse sectors spanning academia, industry, the military and the oil industry itself, including until recently the International Energy Agency or, at least, key individuals or factions therein" are expecting an oil crunch "within a few years," most likely "within a window from 2015 to 2020."

Despite its serious tone, The Energy of Nations: Risk Blindness and the Road to Renaissance, published by the reputable academic publisher Routledge, makes a compelling and ultimately hopeful case for the prospects of transitioning to a clean energy system in tandem with a new form of sustainable prosperity.

The five risks he highlights cut across oil depletion, carbon emissions, carbon assets, shale gas, and the financial sector:

"A market shock involving any one these would be capable of triggering a tsunami of economic and social problems, and, of course, there is no law of economics that says only one can hit at one time."

At the heart of these risks, Leggett argues, is our dependence on increasingly expensive fossil fuel resources. His wide-ranging analysis pinpoints the possibility of a global oil supply crunch as early as 2015. "Growing numbers of people in and around the oil industry", he says, privately consider such a forecast to be plausible. "If we are correct, and nothing is done to soften the landing, the twenty-first century is almost certainly heading for an early depression."

Leggett also highlights the risk of parallel developments in the financial sector:

"Growing numbers of financial experts are warning that failure to rein in the financial sector in the aftermath of the financial crash of 2008 makes a second crash almost inevitable."

A frequent Guardian contributor, Leggett has had a varied career spanning multiple disciplines. A geologist and former oil industry consultant for over a decade whose research on shale was funded by BP and Shell, he joined Greenpeace International in 1989 over concerns about climate change. As the organisation's science director he edited a landmark climate change report published by Oxford University Press.

Leggett points to an expanding body of evidence that what he calls "the incumbency" - "most of the oil and gas industries, their financiers, and their supporters and defenders in public service" - have deliberately exaggerated the quantity of fossil fuel reserves, and the industry's capacity to exploit them. He points to a leaked email from Shell's head of exploration to the CEO, Phil Watts, dated November 2003:

"I am becoming sick and tired of lying about the extent of our reserves issues and the downward revisions that need to be done because of far too aggressive/ optimistic bookings."

Leggett reports that after admitting that Shell's reserves had been overstated by 20%, Watts still had to "revise them down a further three times." The company is still reeling from the apparent failure of investments in the US shale gas boom. Last October the Financial Times reported that despite having invested "at least $24bn in so-called unconventional oil and gas in North America", so far the bet "has yet to pay off." With its upstream business struggling "to turn a profit", Shell announced a "strategic review of its US shale portfolio after taking a $2.1bn impairment." Shell's outgoing CEO Peter Voser admitted that the US shale bet was a big regret: "Unconventionals did not exactly play out as planned."

Leggett thus remains highly sceptical that shale oil and gas will change the game. Despite "soaring drilling rates," US tight oil production has lifted "only around a million barrels a day." As global oil consumption is at around 90 milion barrels a day, with conventional crude depleting "by over four million barrels a day of capacity each year" according to International Energy Agency (IEA) data, tight oil additions "can hardly be material in the global picture." He reaches a similar verdict for shale gas, which he notes "contributes well under 1% of US transport fuel."

Even as Prime Minister David Cameron has just reiterated the government's commitment to prioritise shale, Leggett says:

"Shale-gas drilling has dropped off a cliff since 2009. It is only a matter of time now before US shale-gas production falls. This is not material to the timing of a global oil crisis."

In an interview, he goes further, questioning the very existence of a real North American 'boom': "How it can be that there is a prolonged and sustainable shale boom when so much investment is being written off in America - $32 billion at the last count?"

It is a question that our government, says Leggett, is ignoring.

In his book, Leggett cites a letter he had obtained in 2004 written by the First Secretary for Energy and Environment in the British embassy in Washington, referring to a presentation on oil supply by the leading oil and gas consulting firm, PFC Energy (now owned by IHS, the US government contractor which also owns Cambridge Energy Research Associates). According to Leggett, the diplomat's letter to his colleagues in London reads as follows:

"The presentation drew some gasps from the assembled energy cognoscenti. They predict a peaking of global supply in the face of high demand by as early as 2015. This will lead to a more regionalised oil market, a key role for West African producers, and continued high and volatile prices." More

Special Programme for Adaptation to Climate Change (SPACC) Implementation of Adaptation Measures in Coastal Zones

TECHNICAL NOTE 5C/SPACC-12-05-01 (15 May, 2012)

Implementation of adaptation measures to address the absence of fresh water and coastal vulnerabilities in Bequia, St. Vincent and the Grenadines

The Special Program for Adaptation to Climate Change (SPACC) pilot project “Implementation of adaptation measures to address the absence of fresh water and coastal vulnerabilities in Bequia, St. Vincent and the Grenadines”, was implemented in Bequia, Saint Vincent and the Grenadines by the World Bank, acting as the implementing agency for the Global Environment Fund (GEF), and the Caribbean Community Climate Change Centre (CCCCC), acting as the executing agency.

Background Bequia is the largest of the Grenadines islands, approximately 7 square miles in size, with a population of 4,874 (1991 census). Due to its size and geology, the island has no surface water and no known underground source. Approximately 30% of the island is covered with scrub vegetation of no market significance. The livelihood of the people of Bequia is tied to the surrounding coastal sea. Most natives are fisher folks or sailors. Given the absence of surface water and the calciferous nature of the soil, fresh water resource is a major issue for Bequia. Bequia’s need for water Bequia’s very limited water resources are being threatened by climate change. For people living in Bequia it is clear that dry spells are becoming unusually long, or that the pattern of the rainy season has changed. Water availability to key critical ecosystems is at greater risk as the limited water available is tapped or harvested by households due to the rain water supply systems that no longer meet their water needs. At present, there is no water distribution system in the island of Bequia. Each household has traditionally solved its water supply needs by building individual rain collection systems. It is indicated that up to 30% of the construction cost of a house in Bequia is allocated to the rain harvesting system.

The community and climate change

Of particular concern is the Paget Farms community (Figure 1) where the least wealthy population of the island lives. The entire community relies exclusively on rain water harvesting as the source of potable domestic water. In fact, many of the households in the Paget Farms community, the population targeted by this pilot, are equipped with underground storage that fill during the rainy season. The others utilize one or more glass reinforced plastic tanks that do not always satisfy their needs throughout the season and water supplies have sometimes had to be supplemented by purchase of water transported by barge from Kingstown. Current trends in precipitation confirm what Global Circulation Models predict: there are longer periods of drought, followed by shorter, more intense precipitation events. Moreover, sea level rise is threatening coastal aquifers through saline intrusion. Both factors are already threatening water supply stability for already stressed populations, which in turn Figure 1 : Paget Farm community in Bequia, with Fisheries Complex in the foreground leads to over-exploitation of aquifers and natural resources, endangering the fragile ecosystems and associated biodiversity.

The project: building a carbon neutral reverse osmosis desalination plant

The pilot project in Bequia was aimed at exploring an integrated, sustainable solution to face these challenges: the combination of a renewable, carbon-free energy generation source (photovoltaic system), with a reverse osmosis desalination plant whose input is inexhaustible sea water. The low-maintenance renewable energy source offsets the high energy demand of the plant by providing all the energy required plus some excess energy for the island, with the additional revenue generated covering operation and maintenance costs. This combination has been proven to be both technically and economically viable, and showcases a robust, sustainable approach to the issue, with a very strong replication potential elsewhere in the Caribbean, where similar zones are suffering similar stress. Download PDF

As the report above states that 'Current trends in precipitation confirm what Global Circulation Models predict: there are longer periods of drought, followed by shorter, more intense precipitation events. Moreover, sea level rise is threatening coastal aquifers through saline intrusion.', all Small Island Developing States (SIDS) should be implementing Plan B. A Plan B is necessary from the perspective of energy security. Should the geo-political situation in the Persian Gulf deteriorate the price of petroleum (oil) could rise dramatically making water unaffordable to residents of islands wholly dependant on fossil fuel produced electricity for their water production. The Cayman Islands has no Plan B. The response from the Water Authority, when questioned what their options were if the was a spike in the cost of diesel stated that they would have to raise their cost to the consumer. Editor

Islands and their surrounding near-shore marine areas constitute unique ecosystems often comprising many plant and animal species that are endemic—found nowhere else on Earth.

The legacy of a unique evolutionary history these ecosystems are irreplaceable treasures. They are also key to the livelihood, economy, well-being and cultural identity of 600 million islanders—one-tenth of the world’s population. Read more about the importance of islands.

The theme Island Biodiversity was chosen to coincide with the designation by the United Nations General Assembly of 2014 as the International Year of Small Island Developing States. In addition, the theme was chosen to correspond with the timing ofCOP decision XI/15 paragraph 1(a) “to strengthen the implementation of the Programme of Work on Island Biodiversity”. Read the notification.

|

| Figure 1: Comparing finite and renewable planetary energy reserves (Terawatt-years). Total recoverable reserves are shown for the finite resources. Yearly potential is shown the environmental for the renewables (source: Perez & Perez, 2009a) |

We have, on this planet, vast renewable energy potential: First and foremost, the solar energy resource is very large (Perez et al., 2009a). Figure 1 compares the current annual energy consumption of the world to (1) the known planetary reserves of the finite fossil and nuclear resources, and (2) to the yearly potential of the renewable alternatives. The volume of each sphere represents the total amount of energy recoverable from the finite reserves and the annual potential of renewable sources.

While finite fossil and nuclear resources are very large, particularly coal, they are not infinite and would last at most a few generations. More

The speed of disruptive innovation in the electricity sector has been outpacing regulatory and utility business model reform, which is why they now sometimes feel in conflict.

That disruptive innovation is only accelerating. RMI’s recent report,The Economics of Grid Defection: When and where distributed solar generation plus storage competes with traditional utility service, sets a timeline for utilities, regulators, and others to get ahead of the curve and shift from reactive to proactive approaches. Becoming proactive and deliberate about the electricity system's transformation, and doing so ahead of any fundamental shifts in customer economics, would enable us to optimize the grid and make distributed technologies the integral and valuable piece we believe they can and should be.

When RMI issued The Economics of Grid Defection three weeks ago, our intent was to stretch the conversation among electricity system stakeholders by looking out far enough in the future to discern a point where the rules of the system change in a fundamental way. We used the best available facts to explore when and where fully off-grid solar-plus-battery systems could become cheaper than grid-purchased electricity in the U.S., thus challenging the way the current electricity system operates. Those systems, in fact, don’t even need to go fully off grid. The much less extreme but perhaps far more likely scenario would be grid-connected systems, which could be just as or even more challenging for electricity system operation and utility business models.

The takeaway is this: even under the fully off-grid scenarios we modeled, we have about 10 years—give or take a few—to really solve our electricity business model issues here in the continental U.S. before they begin compounding dramatically. The analysis also suggests we should carefully read the “postcards from the future” being sent from Hawaii today, and take much more interest in how that situation plays out as a harbinger of things to come.

As an institute with a mission to think ahead in the interest of society, consider this a public service message that these issues will crescendo to a point of consequence requiring dramatic and widespread changes well within current planning horizons. For those who are serious about finding solutions, this is also a call to action and a commitment to partnership.

At RMI, much as we pioneered the concepts of the “negawatt,” the “deep retrofit,” and the “hypercar,” we have also defined what it means to be a “think-and-do tank.” It is not enough to do smart analysis. The solutions we champion must be practically tested, broken, fixed, refined, iterated, and ultimately adopted at scale for us to feel satisfied with our work. Partnering with leading companies and institutions is how we prove an alternative path is possible to a world that is clean, prosperous, and secure.

The Transform scenario of our Reinventing Fire analysis, the most preferable outcome of the electricity futures we have examined, described a future for the U.S. electricity system in which 80 percent of electricity is supplied from renewable sources by 2050, with about half of that renewable supply coming from distributed resources. Given the current grid is only a few percent distributed and less than 13 percent renewable (counting a generous allotment of hydropower), we have quite a ways to go.

Achieving that end state requires many changes. Some of those changes already have momentum and likely won’t require intervention, but others will need a kick start or some other form of “strategic acupuncture” encouragement. At RMI, we would certainly prefer that a transition of this scale be orderly and proactive, because having disruption rock the boat of the current system unprepared would undoubtedly leave some combination of shareholders, ratepayers, and taxpayers smarting.

As we look at the future electricity system—the one we need to be building today—we see five critical differences from the present system. Redesigning our regulatory and market models should reflect these emergent needs.

This future still prominently features a robust wires network; defection from the grid would be suboptimal for a number of reasons. We would assert that everyone is better off if we create a future network that is easier to opt in to, rather than opt out of via the risk of defection.

Moreover, distributed resources—the same ones that could but needn’t threaten defection—have the potential to become a primary tool in the planning and management of grid-based distribution systems. Already, we are working with utilities and regulators in several parts of the country in exploring new ways to incentivize electricity distribution companies to take full advantage of distributed resources to reduce distribution system costs, increase resilience, and meet specialized customer needs. Good regulation will reveal value and facilitate transactions that tap that value, thereby increasing the benefit of distributed resources for all.

Our programs at RMI are designed to honor and accelerate progress toward an electricity system that harnesses these distributed investments. Hence, we have parallel and interactive efforts to accelerate the progress of economic, distributed, and low-carbon disruptive technologies (because we believe they have an important and positive role to play in the electricity system of the future), even as we work with utilities, regulators, and other key stakeholders to migrate to new business models that deploy and integrate these resources in ways that maximize the benefits to society as a whole. We think these dual efforts place “creative tension” in the system from which progress manifests.

Our work on disruptive technologies is focused on driving down the economic costs of deploying these systems by stimulating direct cost reductions, improving risk management and access to capital, and building new business models that are either behind the meter or aggregations across meters. To do this, we work specifically to help drive down solar “balance of system costs” through understanding cost reduction opportunities and then working to implement them, through identifying pathways to more market capital and then working with consortia like truSolar and Solar Access to Public Capital to unlock, and through working on issues like microgrids or researching the prospects for alternative asset models with a wide range of partners.

These insights into disruptive models directly inform our dialogue with utilities, regulators, technology providers, and other stakeholders around ways to migrate existing business models. Our most ambitious effort at transformation is the Electricity Innovation Lab (e-Lab), a multi-year, multi-stakeholder initiative focused on rapid prototyping and fast feedback on solutions for the future energy system. This network has issued seminal thought pieces on future business models, surveys of the costs and benefits of solar, and worked directly with stakeholders like the City of Fort Collins and the U.S. Navy to develop perspectives on pieces of future solutions for all. Beyond that, we work directly with utilities such as PG&E and states like Minnesota on one-off engagements to test different ideas together in a way that provides important experience for the “think-and-do” cycle that epitomizes our approach.

We at RMI are committed to expanding and accelerating the capacity to transform the electricity industry to one epitomized by innovation and customer service above all else, in a way that meets environmental, social, and economic demands. Toward this end, we are convening 13 cross-disciplinary teams from across the country in two weeks for our first-ever e-Lab Accelerator, designed specifically to workshop some of the toughest issues facing the industry in the transition to the next electricity system. This is just one of the broader set of commitments that we have made to not just thinking about solutions, but putting them immediately to the test. Therein lies the key to our change model: think and do. Then repeat. More

Caledonian Financial services spent nearly a year transforming their gravel parking lot into Cayman's largest solar farm. The solar carpark has been generating electricity since mid-January, it was officially unveiled at a ceremony Thursday (13 March) night.

“Every minute where the sun is shining, on average, we make 50 cents worth of electricity,” said Caledonian CEO Barry McQuain, “That doesn’t sound like a lot but over the course of a year that adds up to more than $100,000.”

The solar carpark has been generating electricity since mid-January. It was officially unveiled at a ceremony Thursday (13 March) night.

Some 520 photovoltaic panels produce about half the energy Caledonian uses. The solar farm will pay for itself in 5 to 6 years, and has a life span of more than 20.

Caledonian CFO Steven Sokohl breaks it down in banking terms.

“We look at it this way, it’s basically as a bank, we’re giving a loan at 16-17% interest, so what’s not to like about that?” quipped Mr. Sokohl.

Minister of Infrastructure Hon. Kurt Tibbetts applauded Caledonian’s efforts to go green, and urged others to follow their lead. He told the assembled crowd incentives are available to any other business entity or individual who seeks to join the green revolution. More

In late February, Bloomberg finally addressed the most problematic issue in shale gas and tight oil wells: their incredible decline rates and diminishing prospects for drilling in the most-profitable "sweet spots" of the shale plays. I have documented that issue at length (for example, "Oil and gas price forecast for 2014," "Energy independence, or impending oil shocks?," "The murky future of U.S. shale gas," and my Financial Times critique of Leonardo Maugeri's widely heralded 2012 report).

The sources for the Bloomberg article are shockingly candid about the difficulties facing the shale sector, considering that their firms have been at the forefront of shale hype.

The vice president of integration at oil services giant Schlumberger notes that four out of every 10 frack clusters are duds. Geologist Pete Stark, a vice president of industry relations at IHS—yes, that IHS, where famous peak oil pooh-pooher Daniel Yergin is the spokesman for its CERA unit—actually said what we in the peak oil camp have been saying for years: "The decline rate is a potential show stopper after a while…You just can’t keep up with it."

The CEO of Superior Energy Services was particularly pithy: "We've drilled all the good stuff…These are very poor quality formations that I don't believe God intended for us to produce from the source rock." Source rocks, as I wrote last month, are an oil and gas "retirement party," not a revolution.

The toxic combination of rising production costs, the rapid decline rates of the wells, diminishing prospects for drilling new wells, and a drilling program so out of control that it caused a glut and destroyed profitability, have finally taken their toll.

Numerous operators are taking major write-downs against reserves. WPX Energy, an operator in the Marcellus shale gas play, and Pioneer Natural Resources, an operator in the Barnett shale gas play, each have announced balance sheet “impairments” of more than $1 billion due to low gas prices. Chesapeake Energy, Encana, Apache, Anadarko Petroleum, BP, and BHP Billiton have disclosed similar substantial reserves reductions. Occidental Petroleum, which has made the most significant attempts to frack California’s Monterey Shale, announced that it will spin off that unit to focus on its core operations—something it would not do if the Monterey prospects were good. EOG Resources, one of the top tight oil operators in the United States, recently said that it no longer expects U.S. production to rise by 1 million barrels per day (mb/d) each year, in accordance with my 2014 oil and gas price forecast.

When I wrote “Why baseload power is doomed” and "Regulation and the decline of coal power" in 2012, the suggestion that renewables might displace baseload power sources like coal and nuclear plants was generally received with ridicule. How could "intermittent" power sources with just a few percentage points of market share possibly hurt the deeply entrenched, reliable, fully amortized infrastructure of power generation?

But look where we are today. Coal plants are being retired much faster than most observers expected. The latest projection from the U.S. Energy Information Administration (EIA) is for 60 gigawatts (GW) of coal-fired power capacity to be taken offline by 2016, more than double the retirements the agency predicted in 2012. The vast majority of the coal plants that were planned for the United States in 2007 have since been cancelled, abandoned, or put on hold, according to SourceWatch.

Nuclear power plants were also given the kibosh at an unprecedented rate last year. More nuclear plant retirements appear to be on the way. Earlier this month, utility giant Exelon, the nation’s largest owner of nuclear plants, warned that it will shut down nuclear plants if the prospects for their profitable operation don’t improve this year.

Japan has just announced a draft plan that would restart its nuclear reactors, but the plan is "vague" and, to my expert nose, stinks of political machinations. What we do know is that the country has abandoned its plans to build a next-generation "fast breeder" reactor due to mounting technical challenges and skyrocketing costs.

Nuclear and coal plant retirements are being driven primarily by competition from lower-cost wind, solar, and natural gas generators, and by rising operational and maintenance costs. As more renewable power is added to the grid, the economics continue to worsen for utilities clinging to old fossil-fuel generating assets (a topic I have covered at length; for example, "Designing the grid for renewables," "The next big utility transformation," "Can the utility industry survive the energy transition?" "Adapt or die - private utilities and the distributed energy juggernaut" and "The unstoppable renewable grid").

Nowhere is this more evident than in Germany, which now obtains about 25 percent of its grid power from renewables and which has the most solar power per capita in the world. I have long viewed Germany’s transition to renewables (see "Myth-busting Germany's energy transition") as a harbinger of what is to come for the rest of the developed world as we progress down the path of energy transition.

And what's to come for the utilities isn't good. Earlier this month, Reuters reported that Germany’s three largest utilities, E.ON, RWE, and EnBW are struggling with what the CEO of RWE called “the worst structural crisis in the history of energy supply.” Falling consumption and growing renewable power have cut the wholesale price of electricity by 60 percent since 2008, making it unprofitable to continue operating coal, gas and oil-fired plants. E.ON and RWE have announced intentions to close or mothball 15 GW of gas and coal-fired plants. Additionally, the three major utilities still have a combined 12 GW of nuclear plants scheduled to retire by 2020 under Germany’s nuclear phase-out program.

RWE said it will write down nearly $4 billion on those assets, but the pain doesn’t end there. Returns on invested capital at the three utilities are expected to fall from an average of 7.7 percent in 2013 to 6.5 percent in 2015, which will only increase the likelihood that pension funds and other fixed-income investors will look to exchange traditional utility company holdings for “green bonds” invested in renewable energy. The green bond sector is growing rapidly, and there's no reason to think it will slow down. Bond issuance jumped from $2 billion in 2012 to $11 billion in 2013, and the now-$15 billion market is expected to nearly double again this year.

A new report from the Rocky Mountain Institute and CohnReznick about consumers "defecting" from the grid using solar and storage systems concludes that the combination is a "real, near and present" threat to utilities. By 2025, according to the authors, millions of residential users could find it economically advantageous to give up the grid. In his excellent article on the report, Stephen Lacey notes that lithium-ion battery costs have fallen by half since 2008. With technology wunderkind Elon Musk's new announcement that his car company Tesla will raise up to $5 billion to build the world's biggest "Gigafactory" for the batteries, their costs fall even farther. At the same time, the average price of an installed solar system has fallen by 61 percent since the first quarter of 2010.

At least some people in the utility sector agree that the threat is real. Speaking in late February at the ARPA-E Energy Summit, CEO David Crane of NRG Energy suggested that the grid will be obsolete and used only for backup within a generation, calling the current system "shockingly stupid."

Non-hydro renewables are outpacing nuclear and fossil fuel capacity additions in much of the world, wreaking havoc with the incumbent utilities' business models. The value of Europe's top 20 utilities has been halved since 2008, and their credit ratings have been downgraded. According to The Economist, utilities have been the worst-performing sector in the Morgan Stanley index of global share prices. Only utilities nimble enough to adopt new revenue models providing a range of services and service levels, including efficiency and self-generation, will survive.

In addition to distributed solar systems, utility-scale renewable power plants are popping up around the world like spring daisies. Ivanpah, the world's largest solar "power tower" at 392 megawatts (MW), just went online in Nevada. Aura Solar I, the largest solar farm in Latin America at 30 MW, is under construction in Mexico and will replace an old oil-fired power plant. India just opened its largest solar power plant to date, the 130 MW Welspun Solar MP project. Solar is increasingly seen as the best way to provide electricity to power-impoverished parts of the world, and growth is expected to be stunning in Latin America, India and Africa.

Renewable energy now supplies 23 percent of global electricity generation, according to the National Renewable Energy Laboratory, with capacity having doubled from 2000 to 2012. If that growth rate continues, it could become the dominant source of electricity by the next decade.

Faltering productivity, falling profits, poor economics and increasing competition from power plants running on free fuel aren't the only problems facing the fossil-fuels complex. It has also been the locus of increasingly frequent environmental disasters.

On Feb. 22, a barge hauling oil collided with a towboat and spilled an estimated31,500 gallons of light crude into the Mississippi River, closing 65 miles of the waterway for two days.

More waterborne spills are to be expected along with more exploding trains as crude oil from sources like the Bakken shale seeks alternative routes to market while the Keystone XL pipeline continues to fight an uphill political battle. According to the Association of American Railroads, the number of tank cars shipping oil jumped from about 10,000 in 2009 to more than 230,000 in 2012, and more oil spilled from trains in 2013 than in the previous four decades combined.

Federal regulators issued emergency rules on Feb. 25 requiring Bakken crude to undergo testing to see if it is too flammable to be moved safely by rail, but I am not confident this measure will eliminate the risk. Light, tight oil from U.S. shales tends to contain more light molecules such as natural gas liquids than conventional U.S. crude grades, and is more volatile.

Feb. 11 will go down in history as a marquee bad day for fossil fuels, on which 100,000 gallons of coal slurry spilled into a creek in West Virginia; a natural gas well in Dilliner, Pa., exploded (and burned for two weeks before it was put out); and a natural gas pipeline ruptured and exploded in Tioga, ND. Two days later, another natural gas line exploded in the town of Knifely, Ky., igniting multiple fires and destroying several homes, barns, and cars. The same day, another train carrying crude oil derailed near Pittsburgh, spilling between 3,000 and 7,500 gallons of crude oil.

And don't forget the spill of 10,000 gallons of toxic chemicals used in coal processing from a leaking tank in West Virginia in early January, which sickened residents of Charleston and rendered its water supply unusable.

No return

At this point you may think, "Well, this is all very interesting, Chris, but why should we believe we've reached some sort of tipping point in energy transition?"

To which I would say, ask yourself: Is any of this reversible?

Is there any reason to think the world will turn its back on plummeting costs for solar systems, batteries, and wind turbines, and revert back to nuclear and coal?

Is there any reason to think we won't see more ruptures and spills from oil and gas pipelines?

What about the more than 1,300 coal-ash waste sites scattered across the United States, of which about half are no longer used and some are lacking adequate liners? How confident are we that authorities will suddenly find the will, after decades of neglect, to ensure that they'll not cause further contamination after damaging drinking water supplies in at least 67 instances so far, such that we feel confident about continuing to rely on coal power?

Like the disastrous natural gas pipeline that exploded in 2010 and turned an entire neighborhood in San Bruno, Calif., into a raging inferno, coal-ash waste sites are but one part of a deep and growing problem shot through the entire fabric of America: aging infrastructure and deferred maintenance. President Obama just outlined his vision for a $302 billion, four-year program of investment in transportation, but that's just a drop in the bucket, and it's only for transportation.

Is there any reason to think citizens will brush off the death, destruction, environmental contamination of these disasters—many of them happening in the backyards of rural, red-state voters—and not take a second look at clean power?

Is there any reason to believe utilities will swallow several trillion dollars worth of stranded assets and embrace new business models en masse? Or is it more likely that those that can will simply adopt solar, storage systems, and other measures that ultimately give them cheaper and more reliable power, particularly in the face of increasingly frequent climate-related disasters that take out their grid power for days or weeks?

Is there any reason to think the billions of people in the world who still lack reliable electric power will continue to rely on filthy diesel generators and kerosene lanterns as the price of oil continues to rise? Or are they more likely to adopt alternatives like the SolarAid solar lanterns, of which half a million have been sold across Africa in the past six months alone? (Here's a hint: Nobody who has one wants to go back to their kerosene lantern.) Founder Jeremy Leggett of SunnyMoney, who created the SolarAid lanterns, intends to sell 50 million of them across Africa by 2020.

Is there any reason to believe solar and wind will not continue to be the preferred way to bring power to the developing world, when their fuel is free and conventional alternatives are getting scarcer and more expensive?

Is there any reason a homeowner might not think about putting a solar system on his or her roof, without taking a single dollar out of his or her pocket, and using it to charge up an electric vehicle instead of buying gasoline?

Is there any reason to think that drilling for shale gas and tight oil in the United States will suddenly resume its former rapid growth rates, when new well locations are getting harder to find, investment by the oil and gas companies is being slashed, share prices are falling, reserves are getting taken off balance sheets and investors are getting nervous?

I don't think so. All of these trends have been developing for decades, and new data surfacing daily only reinforces them. More

The IEA’s annual World Energy Outlook (WEO) is seen as the most authoritative set of energy scenarios in the world. Yet when we test the forecasts for the growth of renewable energies in the WEO’s main scenario against reality, we find that the WEO consistently comes out too low. Each year from 2006 on the WEO has had to increase its forecast for wind and solar power. Yet each year the WEO predicts the growth of renewables to level off by 2020, for no clear reason. This sends a wrong message to policy makers about the real potential of renewable energy. It is time for the IEA to acknowledge that its assumptions need correcting.

Every year in November, the International Energy Agency publishes its annual World Energy Outlook (WEO). It intends to show the possible directions for our global energy system, with the goal of guiding policy makers in designing their policies and measures. The World Energy Outlook is the most authoritative scenario exercise in the world, and is seen as such by policy and decision makers. It’s not a prediction of the future, but a sketch of possible pathways. The fact that the WEO appears every year makes it possible to assess how well it forecasts the development of renewables in the various scenarios. Looking back is not a favourite activity of scenario builders – they prefer to look forward. But it is instructive if you want to evaluate how well the scenarios hold up against reality. As it happens, the IEA has a sub-programme for Renewable Energy Technology Deployment, IEA-RETD, supported by eight IEA country members, which carried out a limited assessment of the WEO-2013 and earlier editions. The results are very interesting. First the good news. In general, the scenarios are of high quality. That is to say, they generally pass the recommendations made in the IEA-RETD’s scenario guidelines (called “RE-Assume”), which were published last summer and which show policy makers how they should understand energy scenarios and transpose their conclusions into policies. The WEO does well by most criteria, e.g. on transparency. This implies that policy makers should take to heart the WEO’s main conclusion regarding climate change policies: We need to take action that goes much beyond current policies to get anywhere near a safe pathway with respect to energy security and climate change. But the next question for policy makers is: What actions should that be? Here the bad news emerges. The WEO does provide clues about how renewable energy could contribute to the reduction of CO2 emissions, but these clues are absent in the WEO’s main scenario (the “New Policies” scenario). The assumptions about renewable energies used in this scenario and the modelling are based on misconceptions.

We constructed some graphs showing the cumulative installed capacity of both solar and wind power forecast by the WEO from 2006 to 2013. As shown in the graphs below, every year the WEO adjusted its assumptions upwards. In each year from 2006, the reference scenario in the WEO shows higher cumulative capacity than the year before.

What is more, in all the WEOs the growth is expected to slow down from about the year 2020, but for no obvious reason. Our findings confirm what Terje Osmundsen recently wrote in Energy Post about how solar power is portrayed in the WEO. In wind energy the WEO’s adjustments are quite large as well. Hence, it’s not a wild guess that — unless something fundamentally changes — the 2014 WEO reference scenario will again show an upward adjustment of the growth in renewables towards 2035.

WEO’s New Policies Scenario describes the mainstream developments in global energy. These developments put us on a track for a disastrous global warming of more than 3.5°C, according to the WEO. The globally agreed (but not yet operational) target is an upper limit of 2°C. Hence, the IEA also publishes an ‘alternative’ scenario, which shows what actions should be taken to stay within the 2°C limit. This so-called 450 scenario, named after the upper limit of the CO2 concentration in the atmosphere (450 ppm) that still provides a reasonable chance of staying under a 2°C average temperature increase, is regarded as possible but not very likely to happen. According to our retrospective, especially from 2010 onwards, the alternative, 450 scenarios have been much more representative than the reference scenarios when it comes to the actual development of wind energy (and to a lesser extent, of solar power). As can be seen in the graphs below, the projected growth lines quite accurately follow the actual developments. More